Anatomy of an Appraisal Notice

The purpose of this section is to provide a visual representation of the structures and systems within a Notice of Appraised Value (or appraisal notice). This will aid property owners in understanding the organization, function, and relationships of various data, statements and tables.

Important Note

A Notice of Appraised Value (published by FBCAD) is not a Property Tax Statement or Property Tax Bill (distributed by the County Tax Assessor-Collector — per the Local Taxing Entities that are associated with an individual’s property)

Mailing Address & Property Details

Upon opening the envelope and reviewing the 1st page, you will immediately see your Mailing Address and a section including your Property Details.

Click on Image to Expand

- Quick Ref ID – the most commonly used identifier of your property, used by the appraisal district to quickly refer to your account and may begin with an R, M, P, V but always begins with a letter — for example in the format of the following (R00000, M00000, P00000)

- Property ID – also known as a CAD account or referred to as the Geographic ID (0000-00-000-0000-000) of your property.

- Owner Name – the last name, first name of the individual(s) who is listed as the first owner of the referenced property and listed on a property deed.

- Property Description – a brief legal description of the tract of land typically includes smaller divisions identified by a Lot & Block description. It can also reference the abstract it is located within.

- Property Location – the address of a property is located.

- Protest Deadline – the date your appeal is due to be filed.

- Passcode – a string of characters that is used to access your online appeal

- Online Protest Instructions – Step-by-step instructions on protesting your value using the online portal

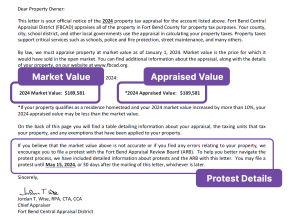

Market Value, Appraisal Value and Protest Details

Further down the 1st page after the introduction, you will see your property’s value according to the market, as of January 1st. Next, you will view the appraisal district’s value for your property.

Click on Image to Expand

- Market Value – the price at which your property could be sold; the price that buyers are willing to pay for your property, according to market conditions.

- Appraised Value – the assessed value generated by the appraisal district, determined following the inclusion of any limitations to the value under the Property Tax Code (such as Homestead, Circuit Breaker, AG Special Valuation, etc.) and if no limitations are present then the Appraised Value is equivalent to the Market Value.

- Protest Details – read important information regarding resolving errors or a disagreement with the appraised value, including the deadline to file.

Review Property Tax Code (Appraisal & Assessment)

Sec. 23.01. APPRAISALS GENERALLY. (a) Except as otherwise provided by this chapter, all taxable property is appraised at its market value as of January 1.

(b) The market value of property shall be determined by the application of generally accepted appraisal methods and techniques. If the appraisal district determines the appraised value of a property using mass appraisal standards, the mass appraisal standards must comply with the Uniform Standards of Professional Appraisal Practice. The same or similar appraisal methods and techniques shall be used in appraising the same or similar kinds of property. However, each property shall be appraised based upon the individual characteristics that affect the property’s market value, and all available evidence that is specific to the value of the property shall be taken into account in determining the property’s market value.

(c) Notwithstanding Section 1.04(7)(C), in determining the market value of a residence homestead, the chief appraiser may not exclude from consideration the value of other residential property that is in the same neighborhood as the residence homestead being appraised and would otherwise be considered in appraising the residence homestead because the other residential property:

(1) was sold at a foreclosure sale conducted in any of the three years preceding the tax year in which the residence homestead is being appraised and was comparable at the time of sale based on relevant characteristics with other residence homesteads in the same neighborhood; or

(2) has a market value that has declined because of a declining economy.

(d) The market value of a residence homestead shall be determined solely on the basis of the property’s value as a residence homestead, regardless of whether the residential use of the property by the owner is considered to be the highest and best use of the property.

(e) Notwithstanding any provision of this subchapter to the contrary, if the appraised value of property in a tax year is lowered under Subtitle F, the appraised value of the property as finally determined under that subtitle is considered to be the appraised value of the property for that tax year. In the next tax year in which the property is appraised, the chief appraiser may not increase the appraised value of the property unless the increase by the chief appraiser is reasonably supported by clear and convincing evidence when all of the reliable and probative evidence in the record is considered as a whole. If the appraised value is finally determined in a protest under Section 41.41(a)(2) or an appeal under Section 42.26, the chief appraiser may satisfy the requirement to reasonably support by clear and convincing evidence an increase in the appraised value of the property in the next tax year in which the property is appraised by presenting evidence showing that the inequality in the appraisal of property has been corrected with regard to the properties that were considered in determining the value of the subject property. The burden of proof is on the chief appraiser to support an increase in the appraised value of property under the circumstances described by this subsection.

(f) The selection of comparable properties and the application of appropriate adjustments for the determination of an appraised value of property by any person under Section 41.43(b)(3) or 42.26(a)(3) must be based on the application of generally accepted appraisal methods and techniques. Adjustments must be based on recognized methods and techniques that are necessary to produce a credible opinion.

(g) Notwithstanding any other provision of this section, property owners representing themselves are entitled to offer an opinion of and present argument and evidence related to the market and appraised value or the inequality of appraisal of the owner’s property.

(h) Appraisal methods and techniques included in the most recent versions of the following are considered generally accepted appraisal methods and techniques for the purposes of this title:

(1) the Appraisal of Real Estate published by the Appraisal Institute;

(2) the Dictionary of Real Estate Appraisal published by the Appraisal Institute;

(3) the Uniform Standards of Professional Appraisal Practice published by The Appraisal Foundation; and

(4) a publication that includes information related to mass appraisal.

Source: Texas Constitution and Statutes

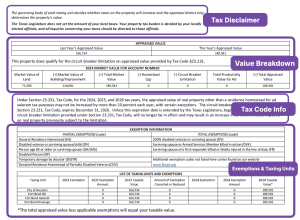

Disclaimer, Breakdown, Tax Code, Exemptions and Taxing Units

On the 2nd page, property owners can review a disclaimer, a table of your property value breakdown, important tax code information, a table of exemption codes, qualifiers, applied exemptions and your local taxing units associated with your property.

Click on Image to Expand

- Tax Disclaimer – regarding your property value and the appraisal district compared to the local taxing units that decide whether to increase property taxes.

- Value Breakdown – a table showcasing comparisons between last year’s appraised value and this year’s appraised value including the market value.

- Tax Code Information – effective limitations and years enacted by the Texas Legislature.

- Exemptions & Taxing Units – exemption codes and any exemptions applied to your property, additionally all local taxing units that ultimately affect your property’s tax burden.

Review Tax Code Information (Circuit Breaker Limitation)

Under Section 23.231, Tax Code, for the 2024, 2025, and 2026 tax years, the appraised value of real property other than a residence homestead for ad valorem tax purposes may not be increased by more than 20 percent each year, with certain exceptions. The circuit breaker limitation provided under Section 23.231, Tax Code, expires December 31, 2026. Unless this expiration date is extended by the Texas Legislature, beginning in the 2027 tax year, the circuit breaker limitation provided under Section 23.231, Tax Code, will no longer be in effect and may result in an increase in ad valorem taxes imposed on real property previously subject to the limitation.

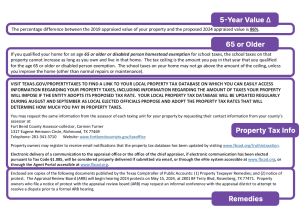

Comparison (In Percentage), OA/DP, Property Tax Information and Remedies

On the 2nd page, property owners can review a disclaimer, a table of your property value breakdown, important tax code information, a table of exemption codes, qualifiers, applied exemptions and your local taxing units associated with your property.

Click on Image to Expand

- 5-Year Value Comparison – The change in property value compared to five years ago, shown as a percentage increase or decrease for this tax year..

- 65 or Older Exemption – refers to tax ceiling while qualified for the OA/DP homestead exemption, which includes disabled persons.

- Property Tax Information – information regarding your local property tax database, contacting the county’s tax assessor-collector and registering for email notifications

- Remedies For Appraisal Value Disputes – documents from the Texas Comptroller of Public Accounts to assist in resolving disputes with appraisal values (not property taxes) — which include Property Taxpayer Remedies and Property Owner’s Notice of Protest.